Its tax season. We just filed our taxes and took a dent to my bank account. One thing tax consultant told us is to maximize 401k contributions. He also made another interesting comment: "You don't know how the laws will change in future, tax rates might differ, govt might cancel Roth IRA. In any case, it is better to save taxes today than later, hence go for traditional 401k"

After the initial mourning phase of the demise of good chunk of bank balance, it made me think, is there a way in which you optimize your 401k contributions in a year that maximizes returns. I am not talking about how much you should contribute, that question is easy: contribute as much as you can up to the maximum that govt allows. I am talking more about how to spread your contributions over the year to maximize the returns from the money.

The usual strategy that most people use, including me, is to contribute x% of your pay check towards 401k, every pay check. Lets call this plan A. Lets say the total amount out of our pay at the end of the year is A$. Now is there any other way to invest A$ but with in a non-uniform spread over the year.

The parameters are:

- Maximum you can contribute towards 401k

- Schedule of your company's matching your contributions

- Your salary

Here is the heuristic approach I chose:

- Contribute every month to get company's contribution

- Chose the maximum amount you can contribute per month

- Calculate the amount you need to contribute to get maximum from the company

- Every month, contribute: minimum( max you can contribute, max you can contribute per year - amount you need to contribute per month to get maximum from company*months remaining in the year - amount contributed so far in the year)

As an example:

- Salary per month: $8000

- max contribution per year allowed (2014 IRS number): $17500

- max you can contribute per month: $4000

- max contribution from the company per paycheck: 50% of your contribution up 6%

- max contribution from the company = $240

- min you need to contribute to get max from company: $480 (6% of 8K)

Depending on this the table of contributions for usual method and the new method looks like this:

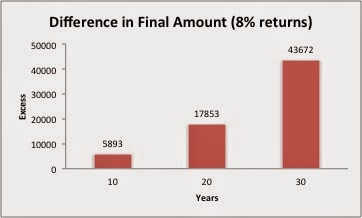

What difference does it make with this contribution? For demonstration purposes, if we assume your 401K portfolio grows at 8% a year, the difference at the end of first year is: $356. Just like that, you have $356 more in your account. If you continue to do this for all your working years, the total savings may look like the following:

Of course it assumes same salary, same contributions, same growth of 401k portfolio, which is an oversimplified assumption, but hey, it shows the point.

In some companies, the employer contribution isn't restricted as what i mentioned above. Some companies pay 100% up to first $x (like QCOM, x = $1500), and then slabs as your contribution grows. The new approach might be much better than old approach in such situations.

Anyway, this is my analysis. If you have any questions, and/or comments on my analysis, I would like to know.

After the initial mourning phase of the demise of good chunk of bank balance, it made me think, is there a way in which you optimize your 401k contributions in a year that maximizes returns. I am not talking about how much you should contribute, that question is easy: contribute as much as you can up to the maximum that govt allows. I am talking more about how to spread your contributions over the year to maximize the returns from the money.

The usual strategy that most people use, including me, is to contribute x% of your pay check towards 401k, every pay check. Lets call this plan A. Lets say the total amount out of our pay at the end of the year is A$. Now is there any other way to invest A$ but with in a non-uniform spread over the year.

The parameters are:

- Maximum you can contribute towards 401k

- Schedule of your company's matching your contributions

- Your salary

Here is the heuristic approach I chose:

- Contribute every month to get company's contribution

- Chose the maximum amount you can contribute per month

- Calculate the amount you need to contribute to get maximum from the company

- Every month, contribute: minimum( max you can contribute, max you can contribute per year - amount you need to contribute per month to get maximum from company*months remaining in the year - amount contributed so far in the year)

As an example:

- Salary per month: $8000

- max contribution per year allowed (2014 IRS number): $17500

- max you can contribute per month: $4000

- max contribution from the company per paycheck: 50% of your contribution up 6%

- max contribution from the company = $240

- min you need to contribute to get max from company: $480 (6% of 8K)

Depending on this the table of contributions for usual method and the new method looks like this:

| Month | New | Old |

| Jan | 4000 | 1458 |

| Feb | 4000 | 1458 |

| Mar | 4000 | 1458 |

| Apr | 1660 | 1458 |

| May | 480 | 1458 |

| Jun | 480 | 1458 |

| Jul | 480 | 1458 |

| Aug | 480 | 1458 |

| Sep | 480 | 1458 |

| Oct | 480 | 1458 |

| Nov | 480 | 1458 |

| Dec | 480 | 1458 |

What difference does it make with this contribution? For demonstration purposes, if we assume your 401K portfolio grows at 8% a year, the difference at the end of first year is: $356. Just like that, you have $356 more in your account. If you continue to do this for all your working years, the total savings may look like the following:

Of course it assumes same salary, same contributions, same growth of 401k portfolio, which is an oversimplified assumption, but hey, it shows the point.

In some companies, the employer contribution isn't restricted as what i mentioned above. Some companies pay 100% up to first $x (like QCOM, x = $1500), and then slabs as your contribution grows. The new approach might be much better than old approach in such situations.

Anyway, this is my analysis. If you have any questions, and/or comments on my analysis, I would like to know.

No comments:

Post a Comment